Monthly Market Update | February 2025

February 2025

Monthly Market Update

Macro Update

-

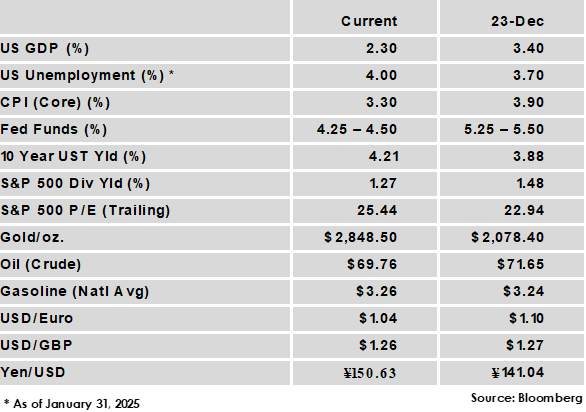

- Growth fears emerged in February as consumer sentiment declined amid policy uncertainty around tariffs, geopolitics, and government cost-cutting. A bitterly cold start to the year for much of the country is also expected to have detracted from activity and be a drag on 1st quarter GDP growth.

- Tariff news continued to dominate headlines as the Trump administration announced that the previously delayed 25% tariffs on Mexico and Canada would take effect on March 4th, with an additional 10% tariff on China and 25% tariffs on steel and aluminum imports also set to take effect in March.

- January’s jobs report saw slightly lower than expected payroll growth, but with upward revisions to prior months the unemployment rate still ticked lower from 4.1% to 4.0%. Wage gains also remained sturdy at 4.1% year-over-year, partly thanks to several minimum wage hike ballot measures that took effect in the new year.

- Inflation results were mixed, with core CPI rising from 3.2% to 3.3% while core PCE, the Fed’s preferred gauge, fell from 2.9% to 2.6%.

Global Equity

-

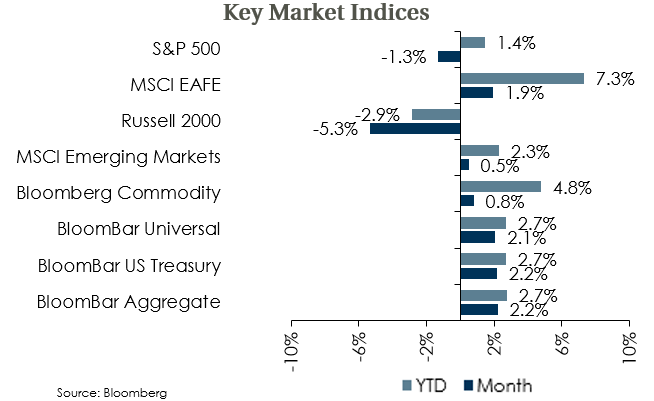

- Equity indices were mixed in February, with US equities lower while non-US equities gained. Non-US developed outperformed as positive economic surprises and the prospect of peace in Ukraine supported returns in Europe. China also performed well as the rise of AI model DeepSeek lifted sentiment in China’s tech sector.

- Trade uncertainty and geopolitics will continue to be a source of equity volatility, and a trade war would likely be a drag on the growth of any involved trading partners. Current forecasts continue to anticipate the US maintaining a growth advantage over most developed market peers, but the gap could narrow.

- S&P 500 earnings have broadened out from the mega-cap leaders and are on track to grow 18% for the fourth quarter, but valuation levels leave little margin for error. Non-US valuations remain below average, and earnings expectations have improved amid ongoing policy easing.

Global Fixed Income

-

- US Treasury yields declined over the latter half of the month as growth and geopolitical concerns weighed on risk sentiment. The 10-year UST yield fell 33 bps in February to 4.21%, the largest monthly decline since July 2024.

- Central bank rate expectations declined in February as Eurozone inflation results supported another ECB cut and US growth concerns added an additional 1-2 Fed rate cuts in 2025 to market based probabilities.

- Credit spreads widened modestly in February, but current spread levels remain historically tight. Total income remains attractive and the strong US economy supports corporate fundamentals, while Absolute Return strategies often benefit from volatility and can offer downside protection in an uncertain environment.

Global Real Estate

-

- Returns for core real estate were positive for the second consecutive quarter in the 4th quarter following two years of declines. Property values appreciated modestly, breaking a nine quarter streak of negative appreciation.

- Cap rates have seen upward pressure in an environment of increased and sticky bond yields. The office sector remains challenged, but could stabilize in the near term as lower construction rates reduce vacancies for existing properties and some firms choose to spend more time back in the office.

|

|

Disclosures and Legal Notice | © 2025 Asset Consulting Group. All Rights Reserved.