Monthly Market Update | January 2023

January 2023

Monthly Market Update

Macro Update

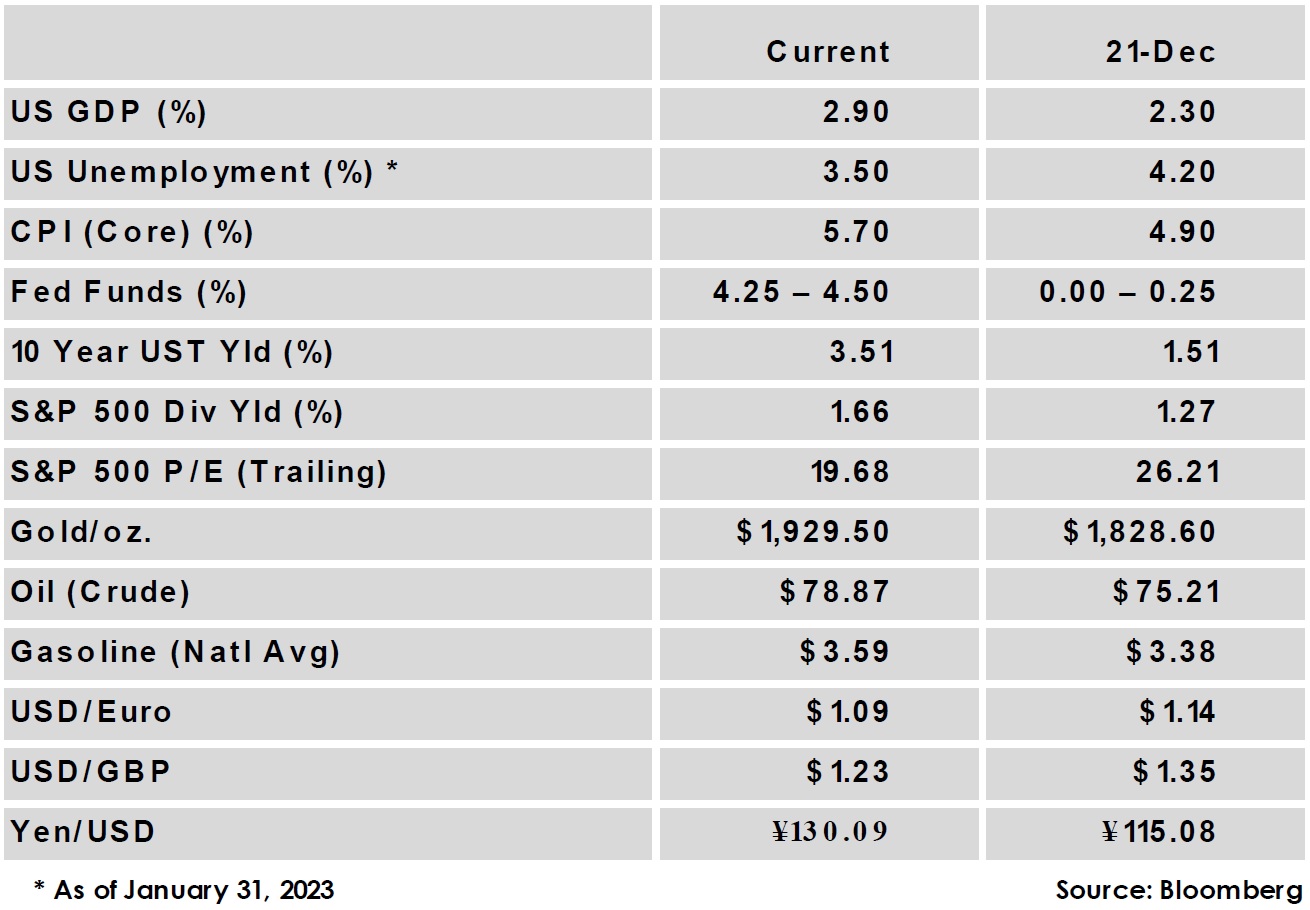

- US growth remained strong with an annualized growth rate of 2.9% in Q4 and 2.1% overall increase for calendar year 2022.

- January data provided the US Fed an opening to step down to a 25 bps hike in early February, with headline CPI declining from an annual rate of 7.1% in November to 6.5% in December, in-line with expectations. Additionally, wage growth declined to a 4.6% year-over-year rate, below expectations.

- Growth in the Eurozone came in above forecast but with a very weak rate of 0.1% quarter-over-quarter in Q4. Calendar year 2022 growth was 3.4%.

- China ended 2022 with GDP growth of 3% vs. the 5.5% official target. However relaxation of zero-Covid policies has raised expectations for stronger growth heading into 2023.

Global Equity

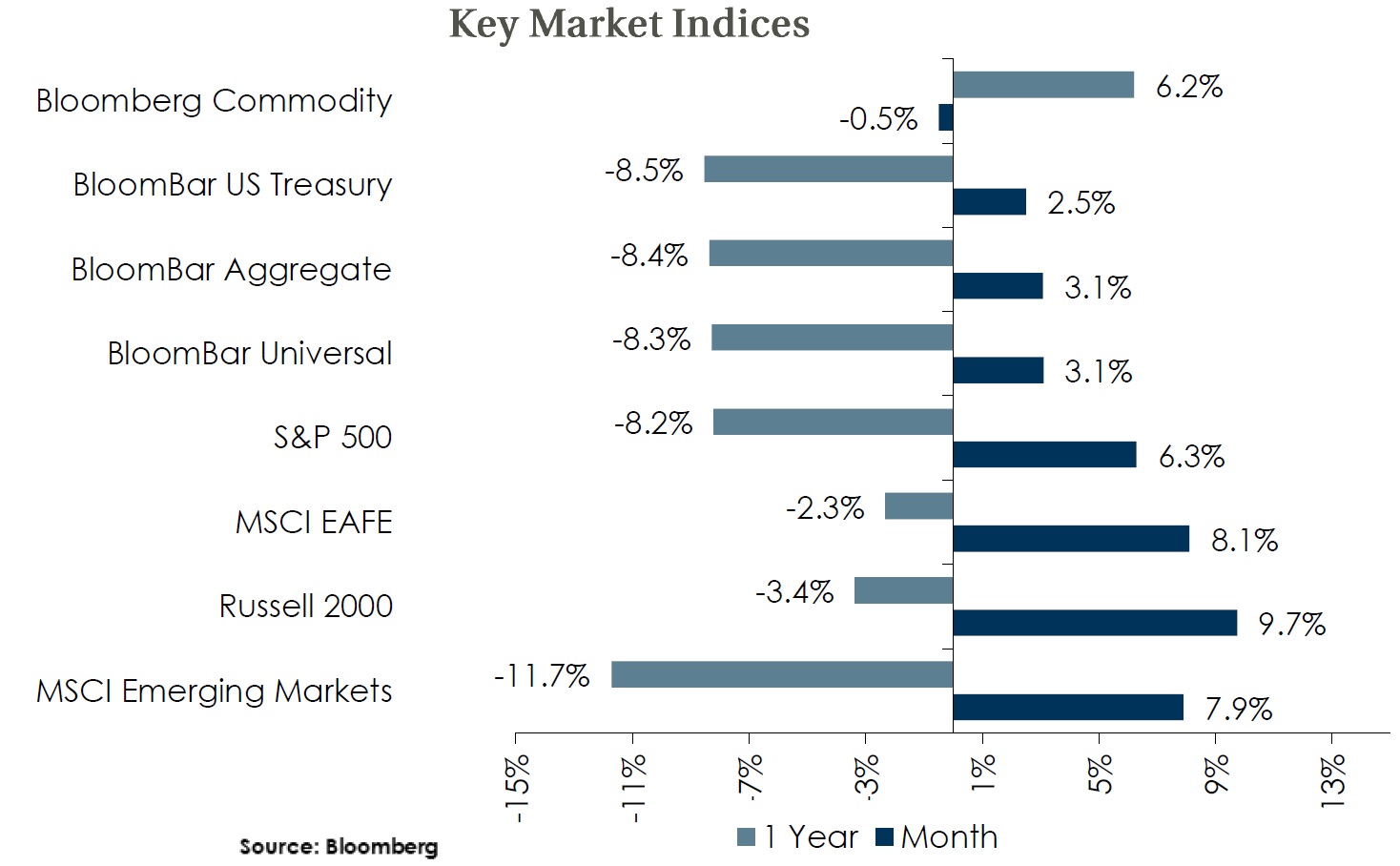

- Equity indices excelled in January as rate hike and inflation fears receded. US Small caps outperformed, followed by non-US and EM with US large caps lagging.

- Growth and tech sectors outperformed as rate sensitive stocks benefitted from a decline in treasury yields and inflation data which pointed to less aggressive central bank policy. Currency helped non-US performance as the US dollar continued its recent reversal.

- Valuations on forward earnings rose in January given the strong performance. Valuations still favor non-US developed equity, and that index also enjoys the strongest recent trend in forward earnings projections.

Global Fixed Income

- Global bond yields fell in January as cooling inflation raised the expectation that most central banks will downshift policy tightening in the near future.

- Credit spreads tightened in the month as high yield moved 49 bps tighter and IG credit 13 bps tighter. Both measures now sit below average but strong fundamentals should help credit weather a slowing economy.

- The 10-year UST yield fell 37 bps, but core bond yields remain elevated relative to recent history.

Global Real Estate

- Core real estate returns continued to decline, turning negative in the 4th quarter for the first time since 2Q 2020.

- Real estate returns could continue to be challenged as higher interest rates put upward pressure on cap rates, which currently sit near historic lows.

|

|

Disclosures and Legal Notice | © 2022 Asset Consulting Group. All Rights Reserved.