Monthly Market Update | January 2025

January 2025

Monthly Market Update

Macro Update

-

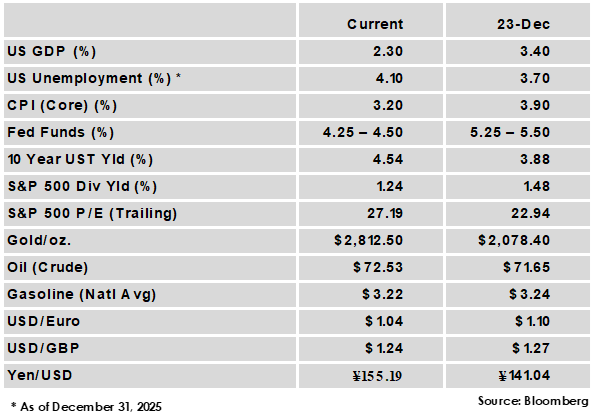

- US GDP grew at a 2.3% annualized rate in the 4th quarter, a solid pace but less than the expected 2.5% rate and a slowdown from the 3rd quarter’s 3.1% pace. For the full year, GDP grew at a 2.8% rate, a slight decline from 2023’s 2.9%.

- The FOMC held its benchmark rate at 4.25% - 4.50%, as expected. Market expectations are for this pause to continue at least through the next meeting in March, and post-meeting statements from Fed Chairman Powell supported that outlook.

- December’s Jobs report exceeded expectations, showing 256,000 jobs added while the unemployment rate fell from 4.2% to 4.1%.

- Inflation continues to be stalled above the Fed’s 2% target, but modest progress was made in December as core CPI declined from 3.3% to 3.2%, slightly better than expected. Core PCE, the Fed’s preferred gauge, held at 2.8% for the third consecutive month.

Global Equity

-

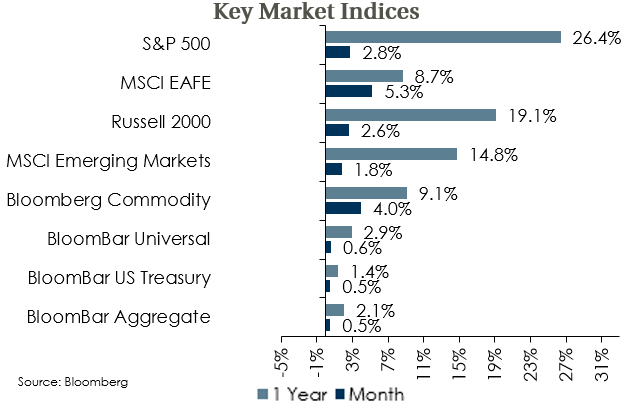

- Equity indices were higher in January, but in departure from recent norms, Non-US developed led and tech stocks underperformed. The US market gained overall even as Chinese AI upstart DeepSeek introduced a model that competes with those from the US and sent many AI related stocks tumbling.

- Equity markets were given a jolt on the last day of the month as the Trump administration said it planned to go forward with 25% tariffs on Canada and Mexico and 10% tariffs on China effective February 1st. US equities declined following the announcement, and trade policy is likely to remain a source of market volatility.

- Earnings at S&P 500 companies are on track to grow 13% for the fourth quarter, the highest since 2021, but valuation levels leave little margin for error. Non-US valuations are reasonable, but the more challenged macro outlook and potential for a trade war dampen upside potential.

Global Fixed Income

-

- US Treasury yields experienced some intramonth volatility but ended January with minimal changes as the Fed meeting brought few surprises and inflation results were near expectations. The US 10-year yield fell 3 bps to 4.54% and the yield curve could remain rangebound with sticky inflation keeping the Fed on hold.

- Policy from other key central banks continued to diverge from the Fed, as the European Central Bank cut rates for a 5th consecutive meeting in January while the Bank of England is expected to cut in early February. Meanwhile, Japan hiked its policy rate to its highest level since 2008.

- Credit spreads tightened in January in both high yield and investment grade bonds, with high yield bonds hitting their tightest level in nearly a year. Current spread levels leave little room for further contraction, but total income remains relatively attractive and the strong US economy supports corporate fundamentals.

Global Real Estate

-

- Returns for core real estate were positive for the second consecutive quarter in the 4th quarter following two years of declines. Property values appreciated modestly, breaking a nine quarter streak of negative appreciation.

- Cap rates have seen upward pressure in an environment of increased and sticky bond yields. The office sector remains challenged, but could stabilize in the near term as lower construction rates reduce vacancies for existing properties and some firms choose to spend more time back in the office.

|

|

Disclosures and Legal Notice | © 2025 Asset Consulting Group. All Rights Reserved.