Monthly Market Update | July 2024

July 2024

Monthly Market Update

Macro Update

-

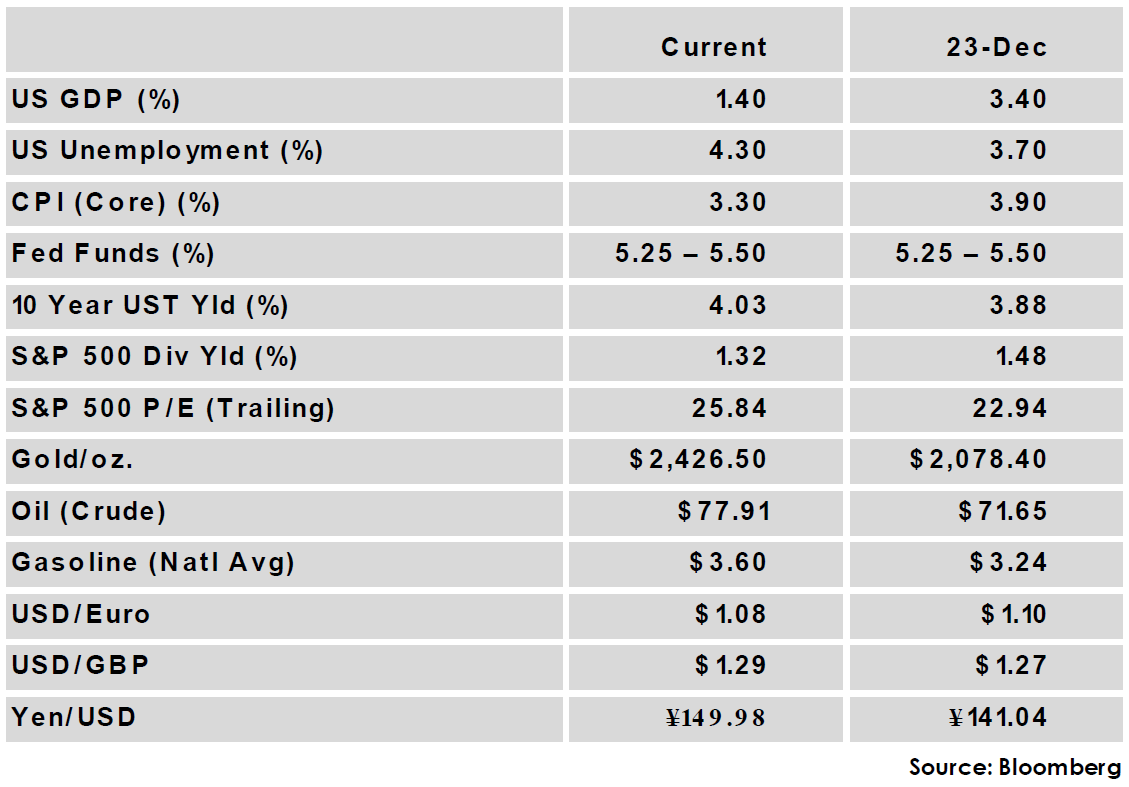

- US GDP growth exceeded expectations, growing at a 2.8% annualized pace in the second quarter. Consumer spending continues to be a key engine for economic growth as personal consumption expenditures contributed over half of the increase.

- The FOMC maintained its benchmark rate at 5.25% - 5.50% at its July meeting, as expected. In the post meeting press conference, Fed Chair Jerome Powell said the committee was open to a September rate cut provided economic data in the next two months was supportive of such a move.

- Inflation eased more than expected as core CPI’s year-over-year increase fell from 3.4% to 3.3%. Headline CPI, which includes volatile food and energy, had its first monthly decline since May 2020, with prices falling -0.1% over the month to ease to a 3.0% year-over-year change.

- The US economy added a solid 206,000 jobs in June, higher than expected, but the unemployment rate ticked up to 4.1% as labor force participation increased.

- Eurozone GDP grew at a 1.2% annualized pace in the second quarter, but disappointing recent PMI figures suggest growth momentum there could be stalling.

- US GDP growth exceeded expectations, growing at a 2.8% annualized pace in the second quarter. Consumer spending continues to be a key engine for economic growth as personal consumption expenditures contributed over half of the increase.

Global Equity

-

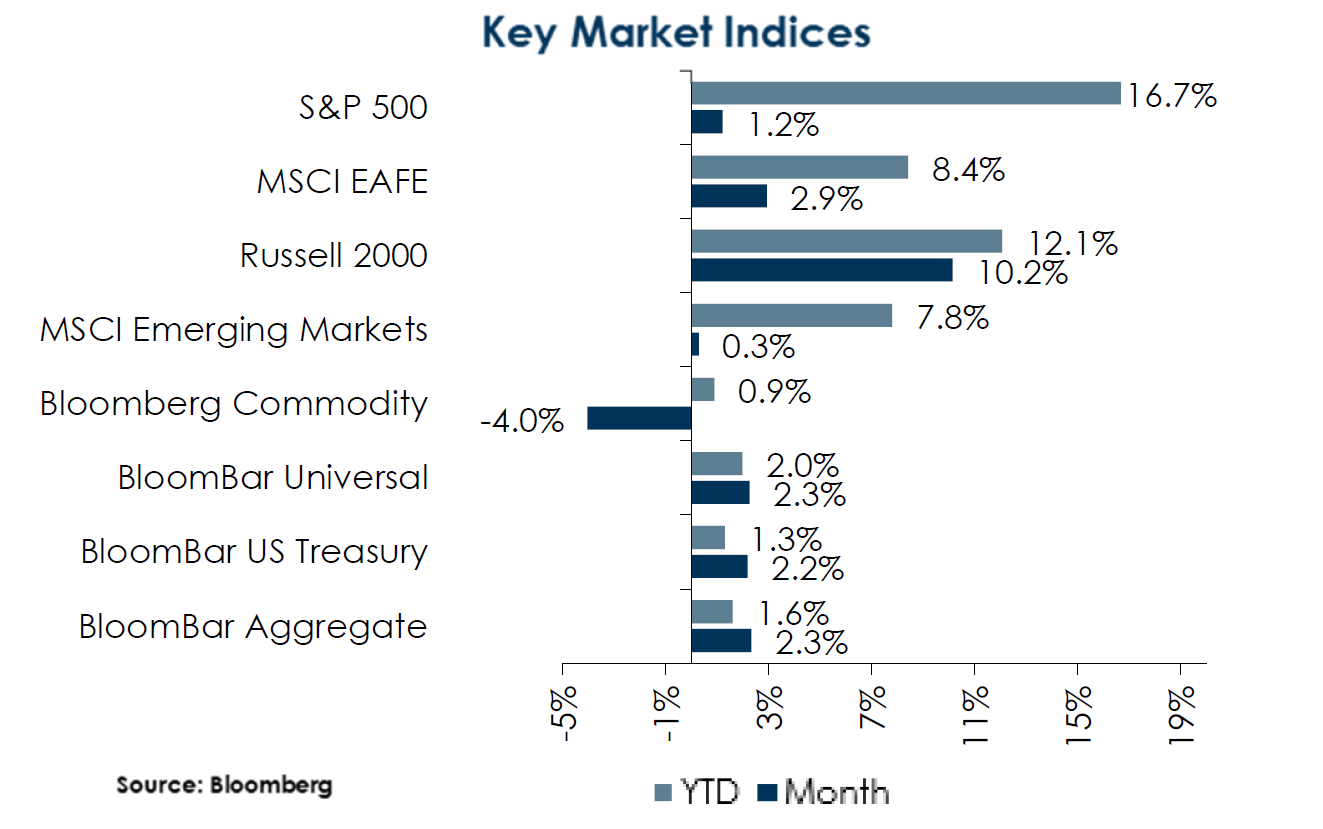

- Equity markets were mostly positive in July but with higher volatility. Emerging market equities were flat while US small caps were clear outperformers as US equities rotated from mega-caps into small/value stocks.

- Currency moves continue to be impactful to non-US returns, as a Bank of Japan rate hike in July helped the Yen gain nearly 7% vs. the USD, boosting EAFE returns.

- Solid earnings and AI enthusiasm remain supportive of US large caps, but shifting sentiment and stretched valuations contributed to the rotation into small caps in July. Markets will continue to grapple with uncertainty around policy, economic growth, and AI profitability, highlighting the importance of diversification.

- Equity markets were mostly positive in July but with higher volatility. Emerging market equities were flat while US small caps were clear outperformers as US equities rotated from mega-caps into small/value stocks.

Global Fixed Income

-

- US treasury yields trended lower for most of the month as inflation and the job market continued to cool and expectations for 2024 rate cuts solidified. Yields were lower across the US Treasury curve and it moved closer to un-inverting as the 10-year yield fell 37 bps to 4.03% while the 2-year yield fell 50 bps to 4.26%.

- Non-US sovereign yields were mostly lower with the exception of Japan as most major central banks are either already easing or nearing a first rate cut.

- Credit spreads continued to trade in a relatively narrow range, with high yield corporate spreads 5 bps wider and IG spreads 1 bps tighter. Both measures are near the bottom of their historic ranges, but the economic backdrop remains supportive of credit and all-in yields are attractive relative to recent history.

- US treasury yields trended lower for most of the month as inflation and the job market continued to cool and expectations for 2024 rate cuts solidified. Yields were lower across the US Treasury curve and it moved closer to un-inverting as the 10-year yield fell 37 bps to 4.03% while the 2-year yield fell 50 bps to 4.26%.

Global Real Estate

-

- Returns for core real estate were negative as market values declined for the eighth consecutive quarter. However more sectors turned positive this quarter as all property types except offices produced positive returns, with office demand continuing to struggle to adapt to post-pandemic work arrangements.

- Cap rates remain under upward pressure in an environment of increased and sticky bond yields. The commercial real estate market is also bracing for a potential surge in loan defaults as existing loans mature and borrowers are forced to refinance at sharply higher rates.

- Returns for core real estate were negative as market values declined for the eighth consecutive quarter. However more sectors turned positive this quarter as all property types except offices produced positive returns, with office demand continuing to struggle to adapt to post-pandemic work arrangements.

|

|

Disclosures and Legal Notice | © 2024 Asset Consulting Group. All Rights Reserved.