Monthly Market Update | March 2025

March 2025

Monthly Market Update

Macro Update

-

- Trade war news remained a focus for investors in March, and financial markets had mixed performance in the month with higher volatility.

- Tariffs on Canada, Mexico, and China went into effect in early March, though exemptions were quickly made for many products following retaliation by the target countries. Trade policy continues to evolve with 25% tariffs on all auto imports announced March 26th and broad “reciprocal” tariffs expected on April 2nd.

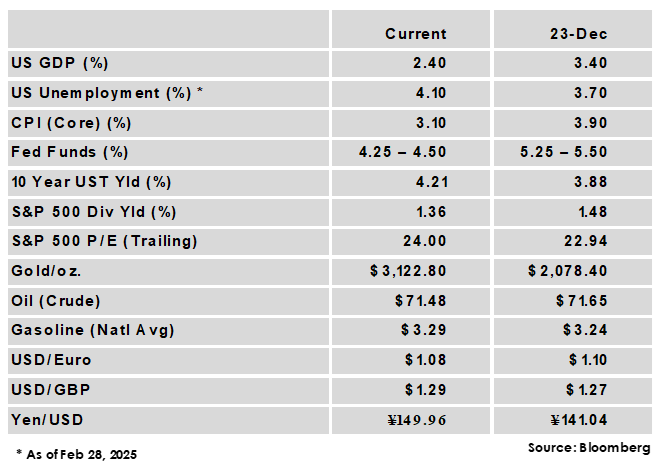

- The US Fed held its benchmark rate steady at a range of 4.25% - 4.50% and maintained forward guidance for two more cuts in 2025.

- Consumer spending rebounded from January’s weather-related decline, but still fell short of expectations with a 0.4% monthly gain.

- The US economy added 151,000 jobs in February, below expectations but in-line with the average monthly gain over the past year.

- Inflation results were mixed as core CPI was lower than expected at 3.1% while core PCE exceeded expectations by ticking higher from 2.7% to 2.8%.

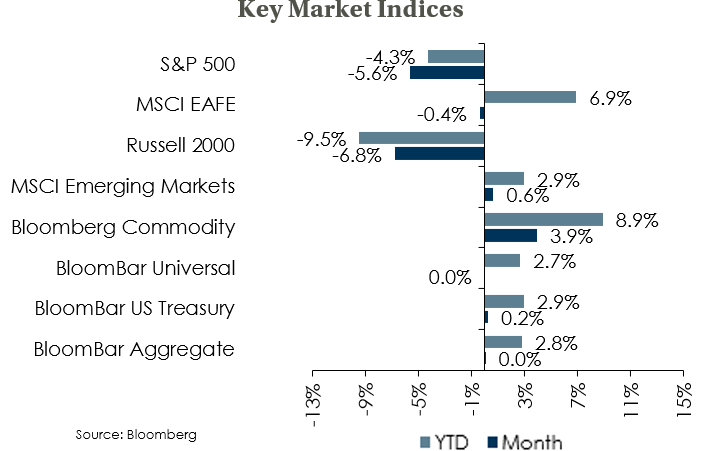

Global Equity

-

- Equity performance was mixed in March, with US equities sharply lower as the S&P 500 hovered near correction territory. Non-US equity markets continued their YTD outperformance as a weaker dollar provided a tailwind, with international developed markets slightly lower and emerging markets positive.

- Trade uncertainty continued to weigh on equity markets and has led to a sharp decline in sentiment. Trade-induced weakness spread to Europe in the month, where indices had their first negative month of the year following the announcement of tariffs on all automobiles not made in the US.

- Prolonged policy uncertainty would increase the risk that negative sentiment becomes a drag on growth. US growth is still forecast to outpace developed market peers in 2025, but with anticipated fiscal support from governments in Europe, that gap looks set to narrow.

Global Fixed Income

-

- US Treasury yields ended the month mixed with a steeper curve as the market digested inflation results, growth concerns, and tariff uncertainty. The 10-year UST yield was flat for the month while shorter tenors declined and the 30-year yield rose.

- Non-US Sovereign yields generally rose in the month, with the 10-Yr German Bund having its largest weekly rise since 1990. Expectations for more fiscal support from Germany and other EU nations has raised the prospects for debt issuance and higher growth for European economies.

-

Credit spreads widened but remain low relative to history. The IG credit spread widened 7 bps while high yield widened 67 to reach its widest point since 2023. Total income remains attractive, while Absolute Return strategies often benefit from volatility and can offer downside protection in an uncertain environment.

Global Real Estate

-

- Returns for core real estate were positive in the 4th quarter, the second consecutive period of gains following two years of declines. Property values appreciated modestly, breaking a nine quarter streak of negative appreciation.

- Cap rates have seen upward pressure in an environment of increased and sticky bond yields. The office sector remains challenged, but could stabilize in the near term as lower construction rates reduce vacancies for existing properties and some firms choose to spend more time back in the office.

|

|

Disclosures and Legal Notice | © 2025 Asset Consulting Group. All Rights Reserved.