Monthly Market Update | November 2024

November 2024

Monthly Market Update

Macro Update

-

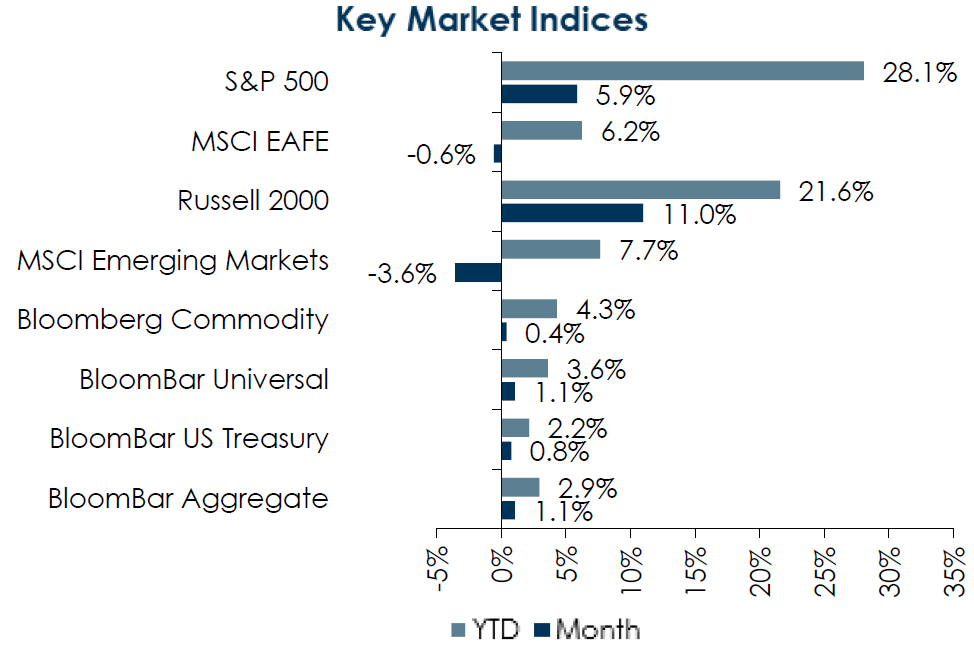

- US Election results were the primary driver of performance in November as markets weighed the implications of a second Trump administration’s policies around tariffs, taxation, regulations, and immigration.

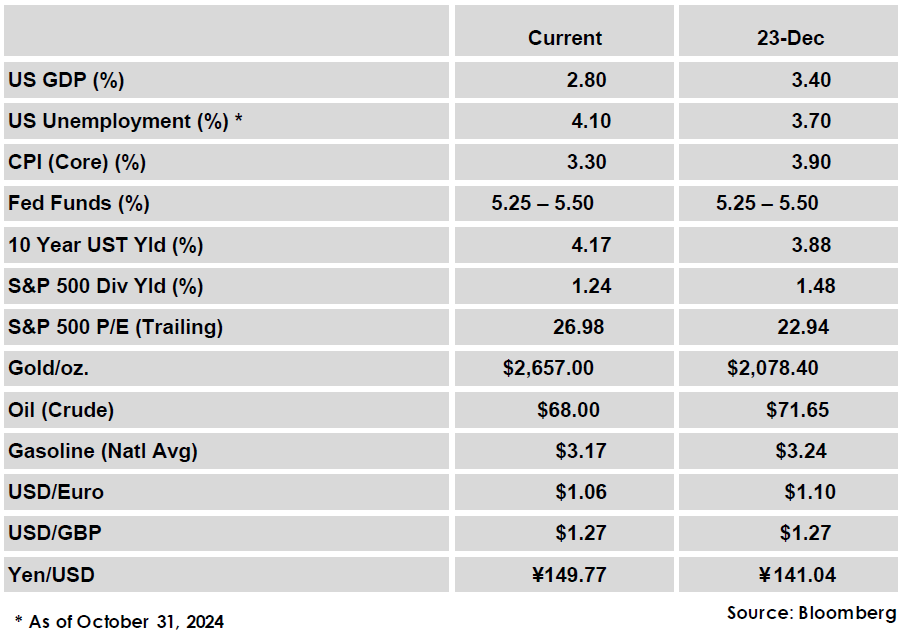

- The FOMC cut rates by 25 bps to 4.50% - 4.75%, as expected. Market forecasts are still uncertain on the December meeting, but are leaning towards another cut.

- Payroll growth was softer in October, partially attributable to labor disputes and back-to-back hurricanes. October’s change in non-farm payrolls was just 12,000, down from September’s 223,000, while the unemployment rate remained steady at 4.1%.

- Inflation remains persistent as Core CPI held steady at 3.3% while Core PCE ticked higher from 2.7% to 2.8%. Still, FOMC meeting minutes continue to strike an optimistic tone with regards to inflation and point to a gradual normalization of interest rates.

Global Equity

-

- Equity markets were mixed in November as investors reacted to election results. US markets outperformed with small caps leading overall as protectionist trade policy is viewed to potentially benefit smaller companies with more US-focused revenue streams.

- The Republican election sweep was regarded as a positive for US growth due to anticipated fiscal easing and deregulation while the potential for higher tariffs was viewed with caution in non-US markets. The US dollar strengthened, further weighing on non-US equity returns.

- Valuations for US equities, particularly large caps, are stretched but earnings forecasts remain solid. Despite the positive US growth outlook, valuation levels leave little margin for error. Non-US valuations are reasonable, but the more challenged macro outlook could dampen upside potential.

Global Fixed Income

-

- US Treasury yields initially climbed in November with expectations of higher inflation and larger fiscal deficits under a second Trump administration. The 10-Yr yield rose as high as 4.45%, but reversed course in the final week of the month to end at 4.17%, down 12 bps on the month.

- Global rates were mostly lower as European sovereign yields declined sharply while in Japan yields rose. Expected monetary policy is somewhat divergent as odds of an additional 2024 rate cut in the US have fallen while the ECB is expected to cut in December and hikes remain on the table in Japan.

- A solid growth outlook continued to support credit spreads in November as IG spreads tightened 6 bps and HY spreads moved 16 bps tighter. Current spread levels leave little room for further contraction, but total income remains relatively attractive and the strong US economy supports corporate fundamentals.

Global Real Estate

-

- Returns for core real estate were positive in the 3rd quarter for the first time since the 3rd quarter of 2022. Property values still declined modestly, but the income component of returns more than made up the difference to generate a positive return overall. All sectors but Offices produced positive returns in the quarter.

- Cap rates have seen upward pressure in an environment of increased and sticky bond yields. With borrowing rates stabilizing and likely to fall, real estate transaction activity is picking up.

|

|

Disclosures and Legal Notice | © 2024 Asset Consulting Group. All Rights Reserved.